Landlords, assets, and equilibrium

Landlords, assets, and equilibrium

A boring one for today

Let’s start off with a quote from – who else? – Marx, writing in Capital Volume 3:

“…a deduction from the average profit or from the normal wages, or both. This portion, whether of profit or wages, appears here as ground-rent, because instead of falling to the industrial capitalist or the wage-worker, as would normally be the case, it is paid to the landlord in the form of lease money. Economically speaking, neither the one nor the other of these portions constitutes ground-rent; but, in practice, it constitutes the landlord's revenue, an economic realization of his monopoly, much as actual ground-rent, and it has just as determining an influence on land prices”.1

Not to be a “the extraordinary prescience of Marx…” guy, but in Volume 3 the extraordinary prescience of Marx with respect to “private property in land” is on full display. Within the passage above is a crucial model of ground-rent as an antagonistic reduction from both the wages of the worker and the profits of the capitalist, and thus the existence of the landlord as a class apart, so to speak. Of course, the landlord is also a capitalist. As I’ve noted tons of times on this Substack, the nominative distinction of “landlord” is relevant at all only when a particular capitalist who owns land-capital appears as a personification of that land-capital in the exchange process. Elsewhere, this personification of land-capital may appear as just a capitalist (‘representing’ another form of capital) or even as a wage-worker. Think of this as seeing a bartender you recognize in the grocery store on a Saturday afternoon. Sure, you may know him as the bartender, but here, he’s just some guy.

Anyway, the relationship of the land-capital owner to workers and owners of other capitals is, I think, a particularly interesting one, riven with antagonisms and cooperation (insofar as the turbulence of capitalist competition allows). Recently I have been reading more about models of housing supply and market equilibrium that treat housing and undeveloped land as assets, and I thought that this could be an instructive little experiment to getting into precisely what I mean with the distinction between land-capital owners and owners of other capitals. Viewing land-capital owners and their activities on the market through this lens suffices to lend some ‘concrete’ heft to the utter immersion in and curious separation of land-capital within larger movements of the market, and in particular, the business cycle.

Assets

The premier approach for housing as an asset is the DiPasquale-Wheaton quadrant model, in which the two create a remarkably elegant arrangement of four curves which make sense of what they diagnose as a meaningful split in the real estate market more broadly, decomposing it into “the market for real estate space and the market for real estate assets”2 This division, however, only holds in the rental market (not just residential, but also in commercial/retail/office/industrial space) as individuals who own and use their land-capital, obviously, encounter the purchase of the asset and ‘access’ to the space as a single transaction. DiPasquale and Wheaton write: “the needs of tenants and the type and quality of buildings available determine the rent for real estate space in the property market. At the same time, buildings may be bought, sold, or exchanged between investors. These transactions occur in the asset or capital market and determine the asset price of space”. Elaborating further, this means that rental prices within a particular local market are determined solely by the market for real estate space (that is, demand), while supply is given pseudo-exogenously from the market for real estate assets.

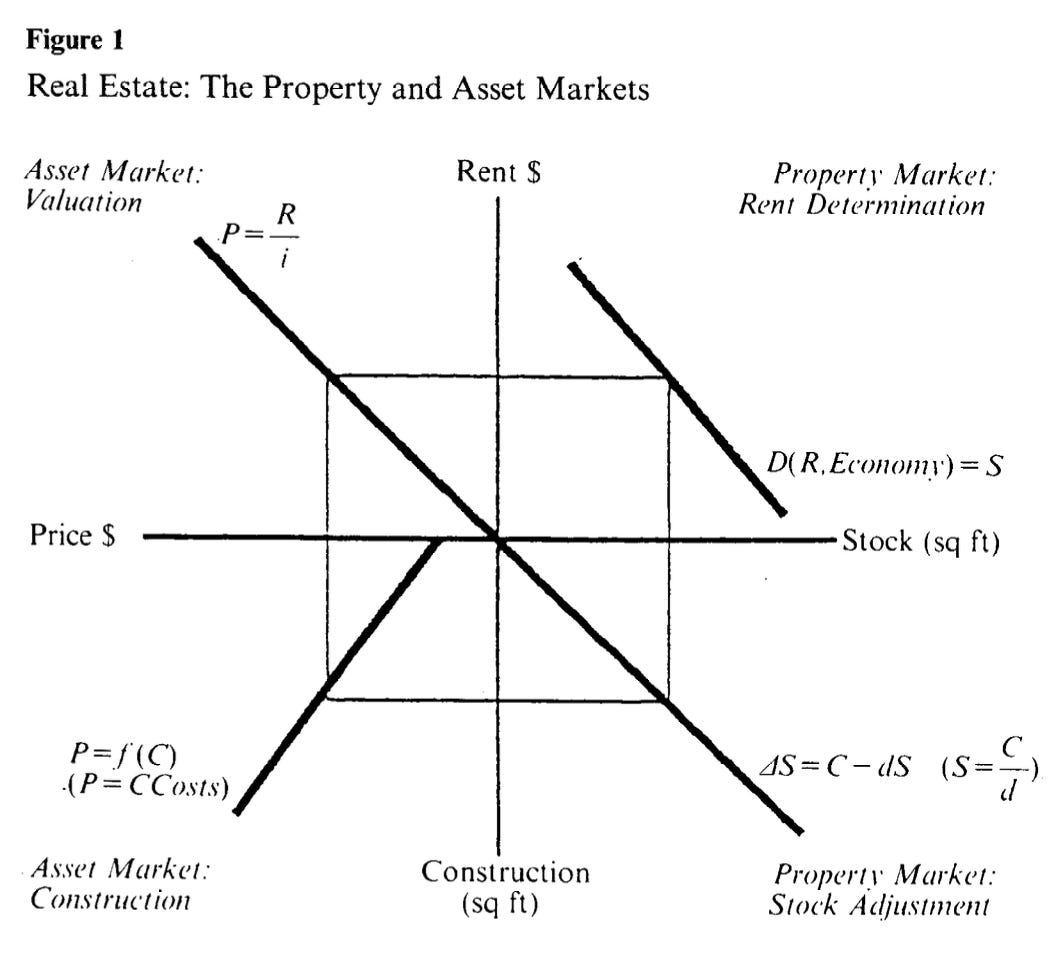

DiPasquale and Wheaton are nice enough to give us this explanatory diagram, which I will quickly summarize (note: read as 4 separate graphs, rotated about the common origin).

In the northwest quadrant, the line represents market equilibrium expressed as the capitalization rate for real estate assets, or the ratio of rent R to price P. Thus the rent level R over capitalization rate i determines price P for real estate assets. This treatment of the cap rate is, however, an object of mild critique – Colwell takes umbrage with the fact that the capitalization rate curve is determined exogenously (DiPasquale and Wheaton cite that it is dependent upon interest rates, expected rent growth, risks in maintaining the asset’s rental stream, and taxation of real estate nationally, as well as, crucially, economy-wide asset market behavior), to say nothing of the obvious epistemic errors in creating a graphical orrery of economic equilibrium, but more on that after I’m done with this description.3

The northeast quadrant illustrates the demand for space, albeit in a rather hilariously incapable fashion viz. an “expanded” demand and supply setup. The authors, assuming equilibrium, find that the demand for space D is equal to the stock of space, S, leaving rent R to be determined so that demand is exactly equal to the stock, leaving the catchall Economy function variable as a sump for any distorting conditions that may distort the curve to the point its fetishistic supply-side ratification would fail. Rent is determined, rather simply, by drawing a vertical line off the horizontal axis until the curve is intersected. Next!

The southwest quadrant is another asset section, this time illustrating a stupid-simple construction market (asset production) calculus in the price obtained from the northwest quadrant, which is extended down into the southwest quadrant until it intersects with the curve here, which represents replacement costs of real estate. Moving horizontally from the intersection point to the vertical axis discovers the amount of new construction where replacement costs equal the asset price from the NW quad: asset price P is equal to construction costs CCosts in a function of construction level f(C): P = CCosts = f(C).

Finally, the southeast quadrant indicates the total flow of construction output which is then converted into real estate stock over a particular period. The change in stock in a particular period ΔS is assumed to be equal to new construction minus losses from removal d (for depreciation), leaving us with ΔS = C - dS. Note here that what is being illustrated is a solid state economy in which construction only produces stock as necessary to replace that which has aged out – that is, equilibrium is only possible within the quadrant and the dual real estate market in general if “the stock of space will be constant over time” and, like all static models, is a simple extrapolative crayon drawing which “determines the value of the stock that would result if that construction continued forever”. Given that stock must remain constant and the northeast quadrant further assumes demand to equal supply at all times, the model closes its literally tautological perambulation by assuring the completion of even its perfect model to be essentially impossible. The authors know this, and offer an unsatisfying caveat: “The combined property and asset markets are in equilibrium when the starting and ending levels of the stock are the same [emphasis mine]. If the ending stock differs from the starting stock, then the values of the four variables in the diagram (rents, prices, construction and the stock) are not in complete equilibrium. If the starting value exceeds the finishing, then rents, prices, and construction must all rise to be in equilibrium. If the initial stock is less than the finishing stock, then rents, prices and construction must decrease to be in equilibrium”. Seems pretty useless, but the model has existed with some tweaks as, if nothing else, a pedagogical tool to propound the virtues of a housing asset market in equilibrium – not unlike the Alonso-Muth-Mills (AMM) which offers about as much utility for actual research, and like DiPasquale and Wheaton’s model, has about the same strained relationship with reality.

The simple introduction of change over time illustrates this destitution further. The authors are aware that their model only offers a general idea of how housing markets in the long-run, but does not make any apology for this long-run merely being a telescoping of existing market conditions barring significant changes in any one of the relevant inputs. In effect, the DiPasquale/Wheaton creation overintellectualizes Schumpeter’s pseudo-dynamic business cycle model, which requires the assumption of a total clearing of all fixed capital at the beginning and end of each business cycle period. Here, the same requirement appears in the assumption that ΔS will always = 0, and thus that the number of households will remain constant in perpetuity. Finally, and most brazenly, the model loses sight of the particularity of the owners of land-capital assets I was stressing earlier. Despite the proclamations of universal models such as this, prices are not arrived at as a simple determination of stock, as shown in the northeast quadrant. On one hand, relevant information of total stock on-market is almost never known by the owner of land-capital looking to turn a rent; on the other, this model offers us essentially nothing for determining price floors and ceilings that would constrain even an owner of land-capital who did enjoy perfect information with respect to the total relevant stock and business activities of other land-capital owners in terms of their price setting. Even the thrilling fiction of Cournot equilibria doesn’t hold here – besides the obvious lack of market standardization which always deranges Cournot models in housing, owners of land-capital have extraordinarily limited market power re: modification of prices through their own price-setting. Fortunately for the parasites, they make up for it in other ways owing to their powers of monopoly over their unique scrap land-capital.

Landlords are evil and stupid

Genesove and Mayer’s (no, it’s not Genovese, I checked) 2001 paper on loss aversion and seller behavior indicates this claim nicely.4 They review the activity of sellers (owners of land-capital entering into the exchange process) in downtown Boston in the 1990s using a modified form of Kahneman and Tversky's "prospect theory", developed in the late 70s as an idealized illustration of utility-maximization qua psychological market decisions made with the threat of risk as a factor.5 They build off a cognizance of the existence of cyclical activity in local and national housing markets with econometric data and surveys of sellers of condos in Boston to arrive at the breathtaking conclusion that "in a boom, houses sell quickly at prices close to, and many times above, the sellers' asking prices. In a bust, however, homes tend to sit on the market for long periods of time with asking prices well above expected selling prices". However, there are further implications that indicate landlords are evil and stupid – in particular, that these owners of land-capital base their primary valuations not on market information at all but rather on past personal experience – that is, the desire to see a return on their investment independent and irrespective of prevailing market conditions. Say, for example, a particular individual purchased a condo in Boston in 1989, at the top of the market. In the early 90s, Boston and the rest of the US experienced a housing crisis which saw prices plummet. If our particular individual wanted to sell their condo in August 1992, as the market was bouncing off the bottom, Genesove and Mayer find that they would likely have “set an asking price that exceeds the asking price of other sellers by between 25 and 35 percent of the percentage difference between the two”. This means that land-capital is nearly always transacted far above its price of production and instead trades at an incremental price, known only to the seller of land-capital, based off of the previous purchase price. This cycle may continue indefinitely barring extreme conditions, constrained only minimally by interest rates, property taxes, etc.

Cameron K. Murray’s work on landbanking and the “housing supply absorption rate” supports this view, extending it to undeveloped land.6 His work highlights, above all, the existence of new land for construction not as an inventory of ready parcels but as assets themselves – another input crucially missing from DiPasquale and Wheaton's model. He describes an economic relationship wherein the land asset is swapped by the owner for a cash asset in an asset market with a finite trading depth – meaning both housing stock supply and incoming pseudo-supply for development is doubly constrained – not only as raw land with a myriad of potential uses, but as an asset contending with other assets in a shallow market. He notes that the evil and stupid behavior described above on its own contributes to an overall increase in land input prices and, if anything, there is a general corrective power which emerges from these individual transactions to drive the price higher: "if the rate of new housing lot sales is higher than this equilibrium ["this equilibrium" = "the marginal cost of selling today equals the marginal benefit in the second period", meaning building, or a cash swap for construction services], there is a benefit from slowing the rate of sales so that the sequence of sales maximizes the present value". Put another way, this means that far from the establishment and maintenance of a particular equilibrium in supply, that supply information is perceived dimly by individual owners of land-capital as something to be constrained. Land assets experience price fluctuations entirely which may be experienced by owners of land-capital as a deleterious signal to draw back their own sales – meaning that there is actually a disadvantage to crowding into a local land asset market experiencing a high rate of sales for an individual owner of a land-capital portfolio. This is entirely in line with Genesove and Mayer's insight above: high price growth in a portfolio delays development precisely because price growth is at the same time asset price growth, and as this land-capital has now seen its price appreciate in the asset market, there is now a limitation to sell for development because the asset valuation of the portfolio has risen.

That is to say again that landlords, this time of a slightly different variant, enjoy a particular relationship to their capital at the beginning and end of every transaction process in a way which is utterly incompatible with the notion of a rational price-setter – even and especially when they trade their land-capital in a ‘fluid’ capital market form such as that with land assets.

In the rental arena, Giacoletti and Parsons find that the “acquisition vintage” bias displayed by owners of land-capital who rent to residential tenants tend to take whether they bought during a boom or during a bust into question in the formation of a rental asking price – noting that land-capital owners who buy on the peak for rental purposes typically charge 2-3% more than those that buy on the trough. There is some literature that combats this finding, citing "sticky rents" instead of the "stale rents" that Giacoletti and Parsons do, but their approach relies on a rather insipid decision game in which the threat of being evicted or not having their lease renewed is recontextualized as the 'power' to exit unilaterally from the transaction with the landlord, resulting in an asset loss for the latter. Their empirical findings are also based on a period of relative stasis in US rental markets (1999-2008) and even then only hold for 1/3rd of renters nationally. Given a landlord's monopoly control over their piece of land-capital, they may function as petty tyrants, untouched by the considerations and assumptions required to make models like DiPasquale and Wheaton's stock-flow game tick. In fact, in the model, they do not appear at all except as utterly rational rubber-stampers of an intelligible, received market price. In reality, each landlord is a jealous god, able to dispose of their property and set rents and asking prices entirely on personal caprice and past experience with the market.

Marx, Karl, and Ernest Mandel. Capital: A Critique of Political Economy, Vol. 3. Translated by David Fernbach. New York, N.Y., U.S.A: Penguin Classics, 1993, p 1265.

DiPasquale, Denise, and William C. Wheaton. “Housing Market Dynamics and the Future of Housing Prices.” Journal of Urban Economics 35, no. 1 (January 1, 1994): 1–27. https://doi.org/10.1006/juec.1994.1001.

Colwell, Peter F. “Tweaking the DiPasquale-Wheaton Model.” Journal of Housing Economics 11, no. 1 (March 1, 2002): 24–39. https://doi.org/10.1006/jhec.2001.0301.

Genesove, David, and Christopher Mayer. “Loss Aversion and Seller Behavior: Evidence from the Housing Market*.” The Quarterly Journal of Economics 116, no. 4 (November 1, 2001): 1233–60. https://doi.org/10.1162/003355301753265561.

Kahneman, Daniel, and Amos Tversky. “Prospect Theory: An Analysis of Decision under Risk.” Econometrica 47, no. 2 (1979): 263–91. https://doi.org/10.2307/1914185.

Murray, Cameron. “Time Is Money: How Landbanking Constrains Housing Supply.” SSRN Scholarly Paper. Rochester, NY, July 10, 2019. https://doi.org/10.2139/ssrn.3417494. and Murray, Cameron K. “A Housing Supply Absorption Rate Equation.” The Journal of Real Estate Finance and Economics 64, no. 2 (February 1, 2022): 228–46. https://doi.org/10.1007/s11146-020-09815-z.